Cash flow is incredibly important to all businesses and cash flow dictates what a business can and cannot do. One of the businesses largest cash outflows is to the ATO whether it be through GST, PAYG quarterly instalments of tax or remitting PAYG Withholding tax withheld from employees’ salary and wages. While the GST and PAYG Withholding are determined as a matter of course, the income tax that your business pays will be dependent on the taxable income at your end.

The following is a brief summary of areas that business owners can consider that will ultimately influence the business taxable income and the amount of tax payable by the business.

Accruing Salary & Wages

It is a good idea to accrue ant unpaid salary or wages incurred between that last pay day and 30 June because this accrual is tax deductible. It is tax deductible because the liability to pay the employee for time worked has already been incurred. For some businesses this may only be a small number but for others it could be substantial.

Bad Debts

Where a debt has been outstanding for some time and you have done everything possible to chase payment of the debt then you can write the debt off as a bad debt and claim a tax deduction for the amount written off provided that:

- the debt was previously included in the assessable income of the business; and

- the debt has been written off. This is normally evidence by a file note or a resolution of the directors.

Further, from a cash flow perspective, you may have debt that is more than 12 months old but you still expect the debt to be paid in full. In such circumstances you have already remitted GST on the debt to the ATO. If the debt is more than 12 months old, you can seek a refund of the GST from the ATO. If you do this and the debtor subsequently pays then you must remit the GST component back to the ATO.

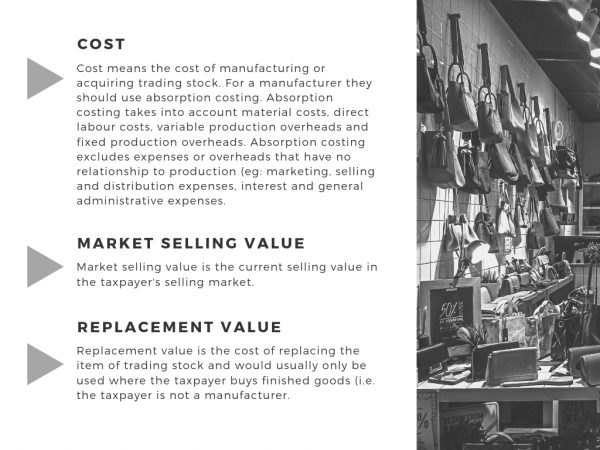

Inventory/Stock

For many businesses stock is a major asset. For this reason, it is good business practice to undertake a stock-take at 30 June to ensure that you have an accurate record of stock on hand.

From a tax perspective, valuing stock for tax purposes can make a significant difference to your tax position. The ATO will accept the following valuation methods for stock:

Based on the 3 options above, cost will normally give you the lowest value for the inventory on hand at 30 June.

If the value of trading stock on hand at 30 exceeds the value of trading stock on hand at 1 July then the excess is assessable and increases your taxable income. Where the trading stock on hand at 30 June is less than the trading stock on hand at 1 July then the difference is deductible and reduces your taxable income.

There is no requirement to apply the same valuation method year on year. You do not have to use the same valuation methodology each year; you may change the method by which you value the stock on hand.

In circumstances where stock is obsolete or defective or past its used by date then you may elect to value these items of stock below cost provided the method of valuation is reasonable.

Superannuation Payments

A business is only entitled to claim a tax deduction for superannuation if the payment has been made within the tax year. Despite the fact that a business incurs a superannuation liability each day a liability to pay an employee arises, the deduction is only crystalised on payment.

Therefor, by 30 June each employer will have incurred a SGC liability equal to 9.5% of its salary and wages bill for the month or quarter. If the business pays this liability in or before 30 June then the expense is deductible in the year in which it is paid. If not paid by 30 June then payment and deduction will fall into the following tax year.

Hence, if cash flow permits, try to pay the employee superannuation on or before 30 June and claim the deduction in the 2019 tax year.

If you do not pay the superannuation contributions prior to 30 June then you need to ensure that the SGC superannuation contributions are pain in full on or before 28 July to ensure you remain eligible to claim a tax deduction in the following year.

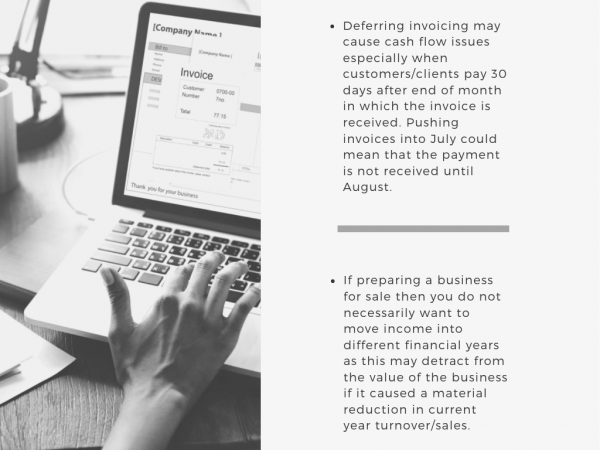

Timing of Income

You may want to consider whether to defer the invoicing of work until after 30 June. While it may push income into the next tax year you also need to assess the commercial aspects which include:

Alternatively, you may have customers/clients that want to be invoiced before 30 June even though the work has not been completed. In these situations you have to assess whether the invoice should be included in the current year or should it be recorded as unearned income and show up in the Statement of Financial Position (Balance Sheet) rather than as a revenue item.

Loans to shareholders & Associates (Division 7A)

For those trading through companies, if the company has lent money to you, a spouse/partner or an associate the you are likely to have a Division 7A loan.

If such a loan or Loans existed at 30 June 2018 then you must ensure that the minimum annual repayment is made on or before 30 June 2019. Failure to make the annual minimum repayment could result in the outstanding balance of the loan being treated as a deemed dividend with no attaching franking credits. This could be an expensive omission.

Further, with significant changes to Division 7A likely in the next 12 months it is worthwhile reviewing the ability to make significant loan repayments in both 2019 and 2020 that the impact of the proposed changes are minimised.

Depreciable Plant and Equipment

Often depreciation schedules get overlooked and new items purchased will be added but plant and equipment lost, stolen, broken or obsolete will continue to to just sit on the depreciation schedule. As such, we would recommend that the depreciation schedule be reviewed and nay piece of plant and equipment not used or too old or damaged to be written off. This will ensure that the accounting depreciation schedule remains relevant and up to date. Subject to any pooling used, there may or may not be a tax benefit involved.

If you are a small business with an aggregated turnover of less than $10m and:

- you purchased a depreciable asset between 1 July 2018 and 28 January 2019 – you can immediately deduct the business portion of the depreciating asset where the cost is less than $20,000*

- you have acquired a depreciable asset between 28 January and 2 April 2019 – you can immediately deduct the business use portion if the depreciating asset cost you less that $25,000*

- you have bought a depreciable aset after 2 April but on or before 30 June – you can immediately deduct the business use portion if the value of the depreciating asset us less than $30,000*

*To be deductible the asset must be used or installed and ready for use by the applicable date.

Prepayment of Expenses

If your business is a small business entity (i.e. a business whose aggregated turnover is less than $10.0M) you are able to prepay expenses and claim an immediate tax deduction for the full amount provided that period ends before 30 June of the subsequent tax year. Examples of expenses that could be prepaid are:

- rent

- interest (but not interest in a loan to acquire real property or share/equity based investments)

- lease payments

- accounting fees

Where you own the business premises in a separate entity (being a related party) and you prepay the rent, the prepayment of rent will be fully assessable income of the related party in the year in which the prepayment is made.

If you would like to discuss any of the above mentioned points when planning your 2019 accounts please contact our office 03 9629 1433.

The comments are closed.