Superannuation Contribution – Personal Deductible Contributions

Each person has an annual concessional superannuation contribution cap limit of $25,000. Contributions that count towards this maximum contribution limit each year are:

a) employer compulsory SGC contributions (9.5% of salary and wages)

b) salary sacrifice contributions paid by your employer

c) personal contributions

Why is superannuation important? Not only does it provide you with a focus on saving for retirement, it also has some short and long term tax benefits. Firstly, from a long term perspective the income and capital growth earned on your superannuation balance is only taxed at 15% while you are saving for retirement and 0% when you begin to draw a pension during your retirement years (up to a maximum balance of $1.6m per person).

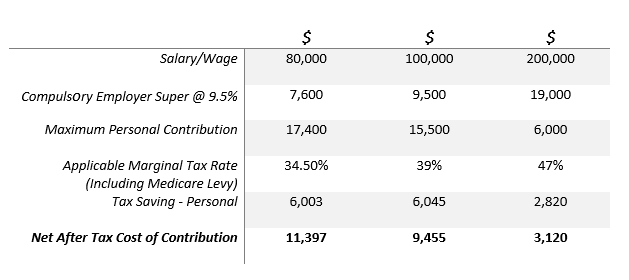

Secondly, by either salary sacrificing or making a personal contribution before 30 June (and claiming a tax deduction in your own income tax return) you are able to reduce your tax. The following is a table setting out the tax benefits of making a personal superannuation contribution before 30 June and claiming a tax deduction in your 2019 tax return:

Not everyone has money in a bank account to call on to put into super. For those who do not but have a loan facility that you can draw on the annualised cost of interest, assuming you contribute the maximum amounts above and make no repayments until 30 June next year, is $730.80, $651.00 and $252 respectively based on 4.2% interest rate.

Ideally, you would use any tax refund to pay down the loan applicable to the contribution and pay the balance off as soon as possible but not later than 30 June next year because you would want to be ready to do it again next year.

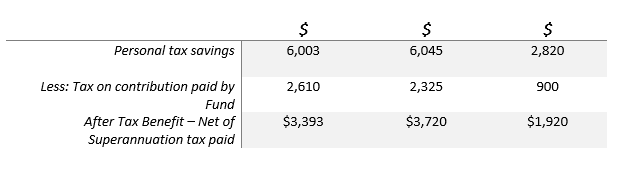

The contribution you make to superannuation for which you are claiming a tax deduction goes into the superannuation fund as a personal concessional contribution and the Fund pays tax on this contribution at the rate of 15% . When factoring this into account the after tax benefit on making the above contributions is as follows:

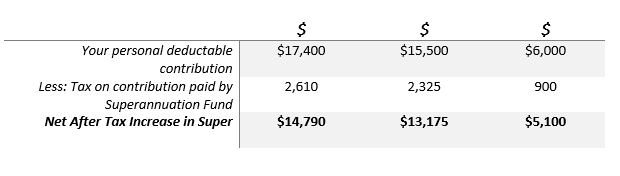

While your net after tax saving is meaningful, you have also increased your superannuation balance by an after tax amount as follows:

When implementing this strategy there are certain things that you need to keep in mind:

- The contribution must be held as cleared funds by the superannuation fund on or before 30 June. If with an industry fund or retail fund you need to check what cut off dates that impose for contributions as the cut offs are normally before 25 June.

- To claim a tax deduction for the personal contribution made you must complete a Notice of Intention to Claim a Tax Deduction form and give to the trustee of the fund. Most industry and retail funds will have these forms on their websites.

- The Notice of Intention to Claim Tax Deduction must be completed before you lodge your 2019 income tax return.

If you would like to discuss this further call 03 9629 1433 or contact us via email

The comments are closed.