Now that we are through another Federal Election and we can all let out a collective sigh of relief knowing that we can still obtain a refund of unused franking credits either personally or through our , that negative gearing is alive and well, that the 50% capitals gains tax discount will remain in place and that we will not face the prospect of possible death taxes. Our attention now turns to year end tax matters and ways in which we can minimise our tax position.

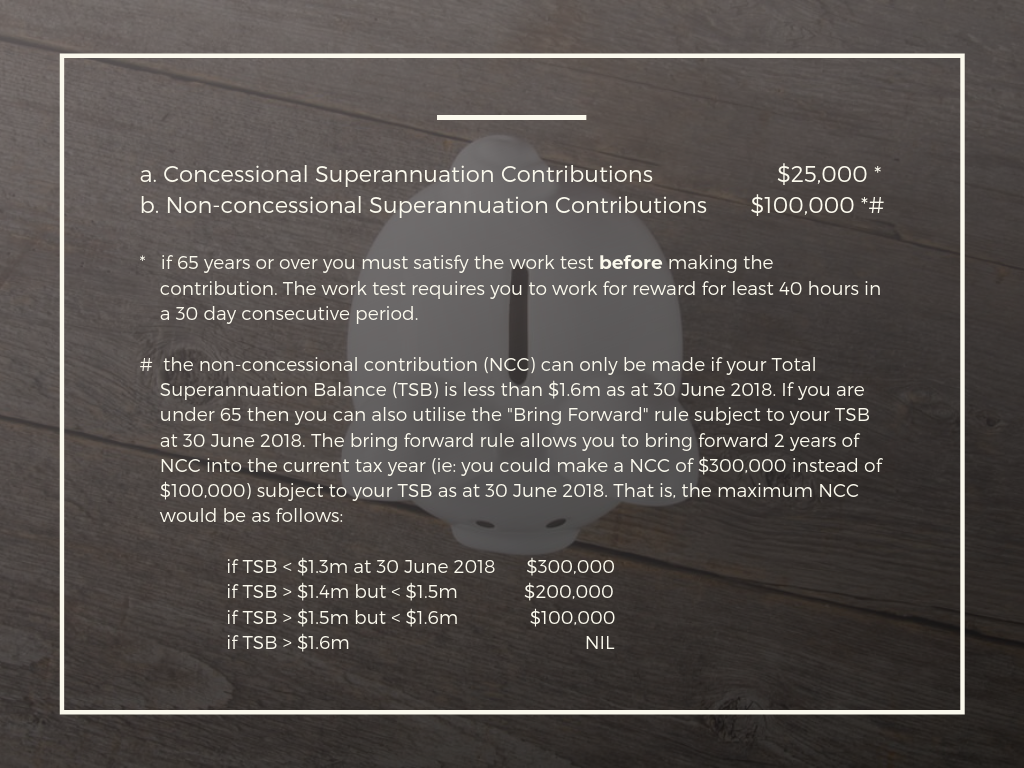

2019 Superannuation Contributions Limits

The maximum contributions for the 2019 tax year are as follows:

You can claim a personal tax deduction for a superannuation contribution provided that you are under the age of 75 and no employer has made a contribution on your behalf in excess of $25,000.

We refer you to our newsletter headed “Year End Superannuation Strategies” for details regarding using personal superannuation contributions to minimise your 2018 tax position.

Capital Gains

If you have sold an asset during the 2019 tax year and have realised a capital gain on the sale of that asset then (apart from the sale of a main residence or a pre-capital gains tax asset) the capital gain is going to be taxable.

Where you have carried forward capital losses then these capital losses can be used to offset a current year capital gain. However, if you do not have any carried forward capital losses then it would be worthwhile reviewing your asset base to see if there are any capital losses that could be released before 30 June to offset any realised capital gains.

It is important to remember that a capital gain is realised when you sign a contract and not when the transaction is settled. This is especially important with property sales. The gain occurs in the year you sign the contract of sale, not the year you settle the sale.

Work Related Deductions

Over the past few years the ATO have increased their audit activity in respect to work related deductions being claimed. As such, even though there is a limit of $300 where substantiation is not required you still must be able to demonstrate that the deduction being claimed was incurred.

Therefore, when claiming any work related deduction we strongly suggest that you maintain receipts as proof that you incurred the expense being claimed.

In relation to some of the common work related expenses being claimed it is worth noting the following:

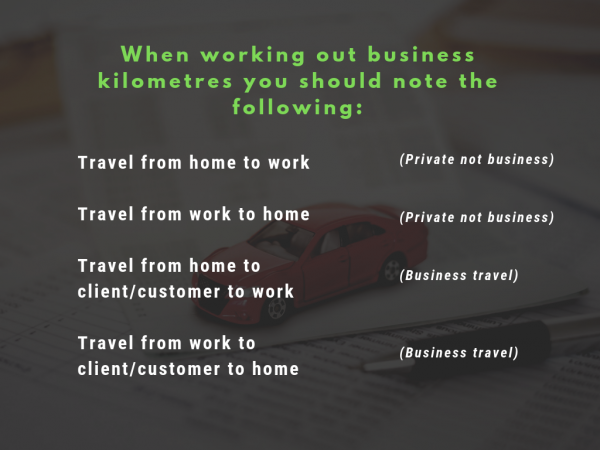

Motor Vehicle Expenses

- If you claim up to 5000 business travel kilometres at a set rate of $0.68 per kilometre. The maximum deduction is $3400. Under the cents per kilometre method you do not need written evidence to show how many kilometres you travelled but, if asked by the ATO, you must be able to justify how you worked out the number of kilometres travelled. Therefore, we suggest you hold a file note setting out how you calculated the number of kilometres travelled.

- If you wish to claim actual motor vehicle expenses incurred you must maintain a log book. The log book must be maintained for 12 consecutive weeks within the tax year and must be representative of your normal business travel. The business use percentage justified by the log book is then applied to the motor vehicle expenses incurred to determine the deduction.

Under the log book method, you must be able to substantiate all expenses incurred.

Subscriptions and Memberships

You are able to claim the cost of any memberships or subscriptions that has a direct connection to your occupation. Examples would include membership to any professional organisation, or union and subscription to trade journals.

Seminars, Conferences & Education Workshops

You can claim the cost of attending any seminar, conference or education workshop provided that there is a connection or nexus between your employment and the seminar, conference or workshop attended.

If your employer has paid for your attendance then you cannot claim a tax deduction as you did not incur the expense.

Clothing, Laundry and Dry-Cleaning Expenses.

You can only claim a tax deduction for the cost of buying and cleaning occupation specific clothing, protective clothing and unique or distinctive uniforms. That is, normal everyday clothing will generally not qualify as being tax deductible.

The cost of uniforms or occupation specific clothing must be capable of being substantiated with written evidence demonstrating that you incurred the expense.

The ATO will allow you to claim $1.00 per load if the load is only work-related clothing or $0.50 per load if you include other laundry in the same load. Where you use a dry-cleaning service, you will need to maintain receipts to evidence that your incurred the expense.

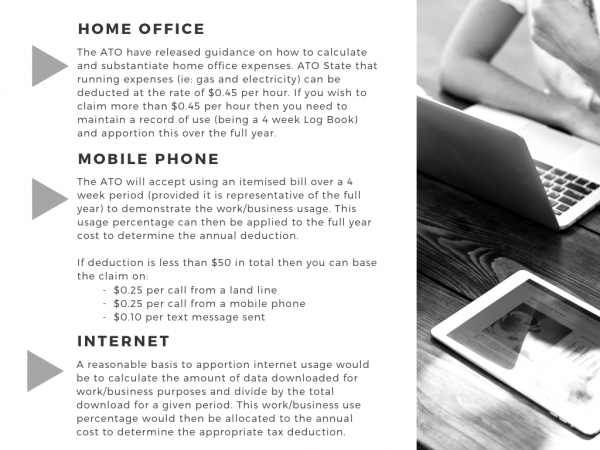

Home Office, Mobile Phone & Internet

The ATO requires you to be able to demonstrate that there is a connection between the claiming of the expense and your income producing activity. The legislation specifically states that you can claim a deduction to the extent that it was incurred in gaining or producing your assessable income. This means that an expense may be apportioned where part use relates to work/business and part is private use.

Prepayment of Expenses

Individual tax payers are able to claim a deduction for prepaying a deductible expense. To be eligible to claim a prepaid expense deduction the expenditure must:

a. be deductible in nature; and

b. be prepaid for a period of not more than 12 months with the prepayment period ending before 30 June of the tax year subsequent to the tax year in which the payment is made.

Examples of deductible expenses would be:

- prepaying interest on an investment property loan

- prepaying interest on a margin loan

- paying an annual premium for an income protection policy (as opposed to paying monthly)

- Prepaying for travel, accommodation and registration fees to attend a seminar or conference.

It should also be noted that the prepayment rules do not apply to excluded expenditure that may enable you to claim a full deduction are:

- if the expenditure is less and $1000. Examples would include professional membership fees, annual subscription fees to professional/trade journals, etc.

- if the expenditure is required to be made by law or pursuant to a court order. An example would be car registration fees.

If you would like to discuss any of the above mentioned points when planning your 2019 tax documents please contact our office 03 9629 1433.

The comments are closed.